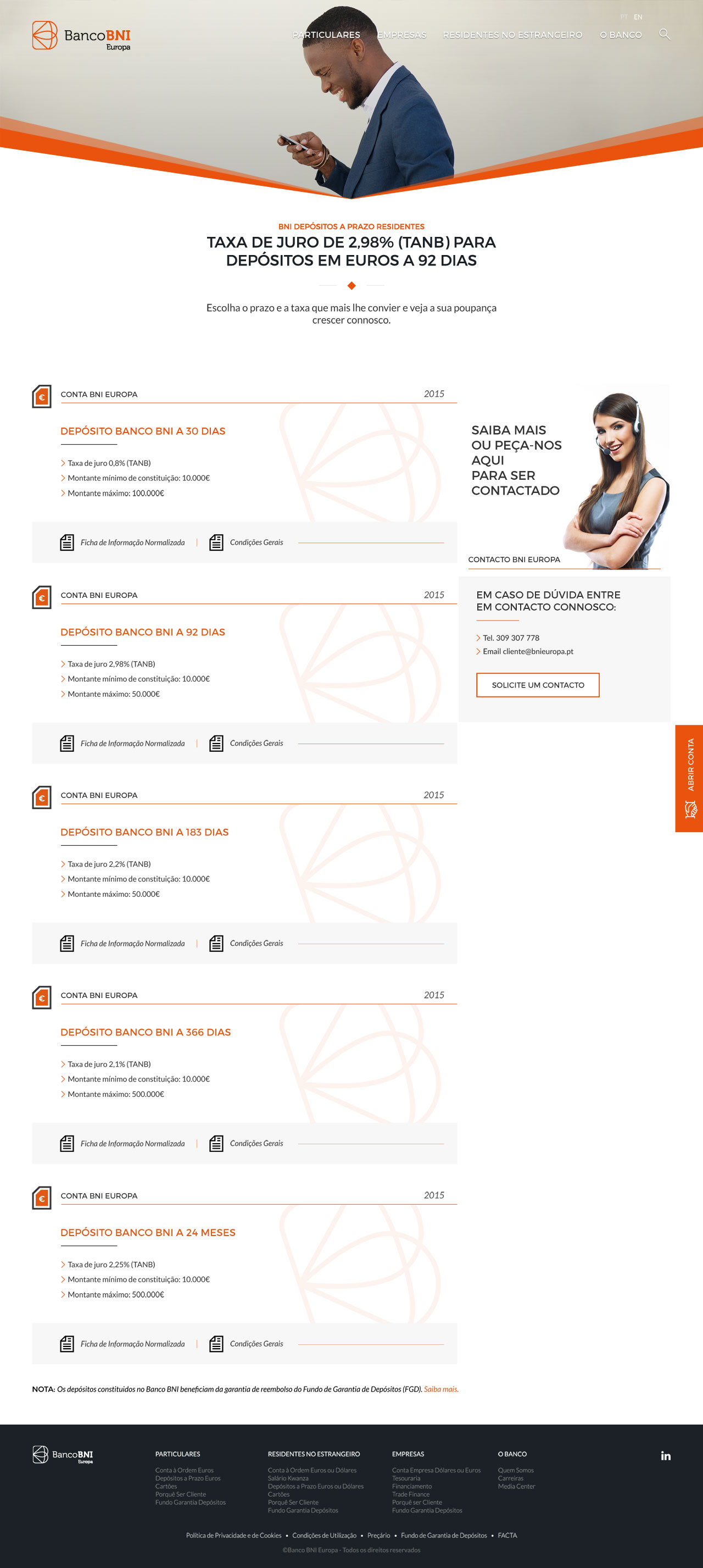

APR calculated based on a Variable Nominal Annual Rate of 5.215% (6 month Euribor from June 2024 of 3.715% and a spread of 1.5%), for a standard loan of 65,000 EUR over 20 years, for a borrower aged 40 with a loan-to-value ratio of 64%. The loan is repayable in 240 monthly installments of principal and interest, with an estimated monthly amount of 436.73 EUR. Total cost of loan is 46,652.67 EUR, and the total amount payable by the consumer (MTIC) is 111,652.67 EUR. This includes: property appraisal fee, initial commissions, contract formalization expenses, stamp duty on credit usage, and insurance premiums for life and multi-risk insurance.

APR calculated based on a Variable Nominal Annual Rate (APR) of 7.701% (6 month Euribor of June 2024 of 3.715% and spread of 3.986%), for a standard loan of 62,500 EUR over 20 years, for a borrower aged 40 with a loan-to-value ratio of 64%. The loan is repayable in 240 monthly installments of principal and interest, with an estimated monthly amount of 511.21 EUR. Total cost of loan is 66,180.45 EUR and total amount charged to the consumer (MTIC) 128,680.45 EUR. Includes: property appraisal fee, initial fees, contract formalization expenses, stamp duty on the use of credit, and life and multi-risk insurance premiums.